本文主要从以下几个方面介绍如何将时间序列的预测转化为有监督的机器学习问题:

- 数据预处理(数据转换、缺失值、异常值)

- 特征提取(窗口特征、日期特征、时间偏移特征)

- 模型检验(时间序列的交叉验证)

数据预处理

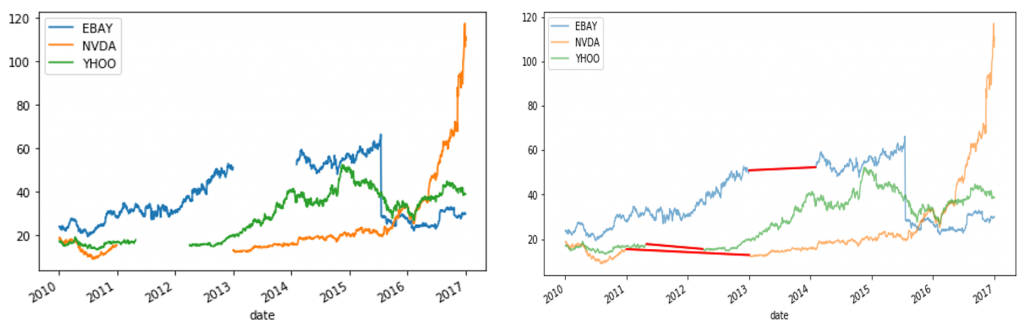

第一步先对时间序列进行观察,看其是否存在缺失值,并结合实际情况对缺失值进行处理或填充。使用的数据下载可点击此处,提取码为fgwa

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

prices = pd.read_csv("data.txt",sep='\s+')

prices['date']=pd.to_datetime(prices['date'])

prices = prices.set_index('date')

prices.plot(legend=True) #左图

plt.tight_layout()

plt.show()

### 对缺失值进行时间插值

def interpolate_and_plot(prices, interpolation):

# Interpolate the missing values

prices_interp = prices.interpolate(interpolation)

# Plot the results

fig, ax = plt.subplots(figsize=(10, 5))

prices_interp.plot(alpha=.6, ax=ax, legend=True)

# Now highlight the interpolated values in red

missing_values = prices.isna() # Create a boolean mask for missing values

prices_interp[missing_values].plot(ax=ax, color='r', lw=2, legend=False)

plt.show()

return prices_interp

# Interpolate linearly

interpolation_type = "linear"

prices = interpolate_and_plot(prices, interpolation_type) #右图

可以看出这三个序列都具有比较明显的不平稳特征,可以进行一定的转换减弱序列的不稳定性。因为数据是股票价格数据,这里使用Pandas中的rolling函数将当前价格转换为当前价格较前一段时间平均价格的增长率。经过转换后也可以更容易地看出异常点所在。

def percent_change(series):

# Collect all but the last value of this window, then the last value

previous_values = series[:-1]

last_value = series[-1]

# Calculate the % difference between the last value and the mean of earlier values

percent_change = (last_value - np.mean(previous_values)) / np.mean(previous_values)

return percent_change

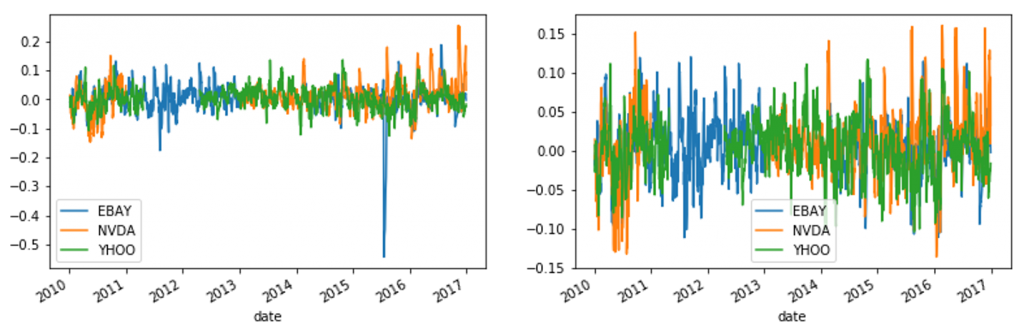

### Apply rolling window and plot

prices_perc = prices.rolling('20d', closed='both').apply(percent_change)

prices_perc.plot() #下方左图

plt.show()

若数据落在距离均值的三个标准差之外,则判断为异常点。异常点的判断方法有很多,这里仅选用这一简单的准则用做说明。

def replace_outliers(series):

# Calculate the absolute difference of each timepoint from the series mean

absolute_differences_from_mean = np.abs(series - np.mean(series))

# Calculate a mask for the differences that are > 3 standard deviations from zero

this_mask = absolute_differences_from_mean > (np.std(series) * 3)

# Replace these values with the median accross the data

series[this_mask] = np.nanmedian(series)

return series

# Apply the function to the timeseries and plot the results

prices_perc = prices_perc.apply(replace_outliers)

prices_perc.plot() #下方右图

plt.show()

特征提取

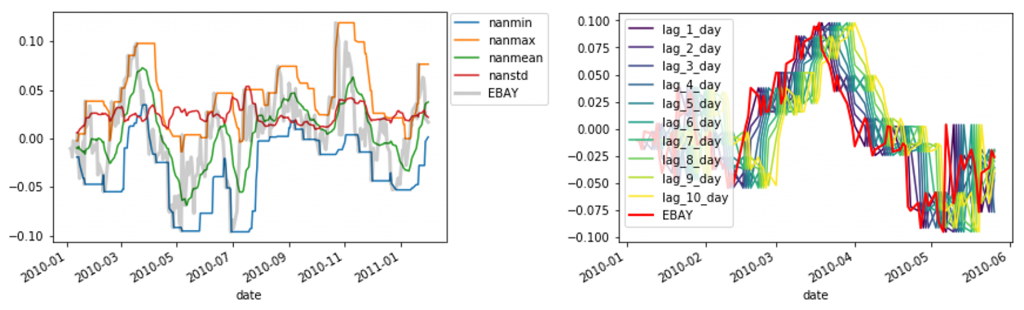

使用Pandas中的rolling函数进行窗口特征的提取,需要注意的是计算窗口特征时不能包含窗口最右边的点,否则提取的特征中就会包含了预测值本身的信息。因此需要将窗口设置为左闭右开的区间 (即参数closed="left")。以EBAY这一列为例:

# Define a rolling window with Pandas, excluding the right-most datapoint of the window

prices_perc_rolling = prices_perc['EBAY'].rolling("20d", min_periods=5, closed='left')

# Define the features that calculate for each window

features_to_calculate = [np.nanmin, np.nanmax, np.nanmean, np.nanstd]

# Calculate these features for rolling window object

features = prices_perc_rolling.aggregate(features_to_calculate)

# Plot the result

ax = features.loc[:"2011-01"].plot()

prices_perc['EBAY'].loc[:"2011-01"].plot(ax=ax, color='k', alpha=.2, lw=3) #下方左图

ax.legend(loc=(1.01, .6))

plt.show()

如果窗口特征的计算中需要传入参数,可使用partial函数

# Import partial from functools

from functools import partial

percentiles = [1, 10, 25, 50, 75, 90, 99]

# Use a list comprehension to create a partial function for each quantile

percentile_functions = [partial(np.nanpercentile, q=percentile) for percentile in percentiles]

# Calculate each of these quantiles on the data using a rolling window

prices_perc_rolling = prices_perc['EBAY'].rolling("20d", min_periods=5, closed='left')

features_percentiles = prices_perc_rolling.aggregate(percentile_functions)

除去窗口特征外,还可以直接对日期信息进行处理获得新的特征,例如:

prices_perc['day_of_week'] = prices_perc.index.dayofweek prices_perc['week_of_year'] = prices_perc.index.weekofyear prices_perc['month_of_year'] = prices_perc.index.month

除去窗口特征和日期特征外,还可以直接使用离预测时刻最近的过去几个时刻的值作为特征,使用Pandas中的shift函数构建时间偏移特征。

# These are the "time lags"

shifts = np.arange(1, 11).astype(int)

# Use a dictionary comprehension to create name: value pairs, one pair per shift

shifted_data = {"lag_{}_day".format(day_shift): prices_perc['EBAY'].shift(day_shift) for day_shift in shifts}

# Convert into a DataFrame for subsequent use

prices_perc_shifted = pd.DataFrame(shifted_data)

# Plot the first 100 samples of each

ax = prices_perc_shifted.iloc[:100].plot(cmap=plt.cm.viridis) #下方右图

prices_perc['EBAY'].iloc[:100].plot(color='r', lw=2)

ax.legend(loc='best')

plt.show()

# Replace missing values with the median for each column

X = prices_perc_shifted.fillna(np.nanmedian(prices_perc_shifted))

y = prices_perc.fillna(np.nanmedian(prices_perc))['EBAY']

模型检验

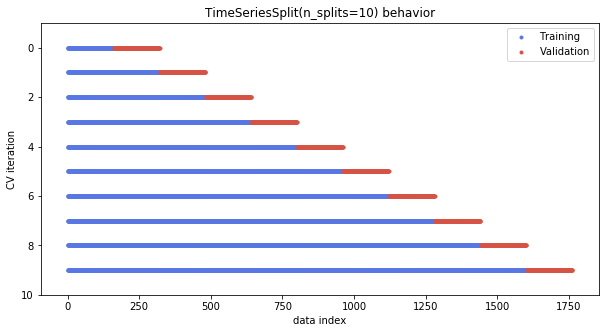

使用sklearn中的TimeSeriesSplit进行模型的交叉检验,不同于一般的交叉检验,时间序列的交叉检验中验证集始终在训练集之后,如下图所示:

由于时间序列的交叉验证的特殊性,可以将所有交叉验证的结果看作一个时间序列:

from sklearn.model_selection import TimeSeriesSplit

cv = TimeSeriesSplit(n_splits=100) #Initialize the cross-validation iterator

scores_time = []

for ii, (tr, tt) in enumerate(cv.split(X, y)):

start_val = tt[0]

scores_time.append(X.index[start_val]) #the start datetime for each validation set

在交叉验证时可以使用自定义的指标来衡量模型的好坏,同时可以使用bootstrap方法来衡量模型的不确定性:

from sklearn.utils import resample

def bootstrap_interval(data, percentile, n_boots=100):

"""Bootstrap a confidence interval for the mean of a 1-D dataset."""

# Create empty array to fill the results

bootstrap_means = np.zeros(n_boots)

for ii in range(n_boots):

# Generate random indices for data with replacement, then take the sample mean

random_sample = resample(data)

bootstrap_means[ii] = random_sample.mean()

# Compute the percentiles of choice for the bootstrapped means

data_percentile = np.percentile(bootstrap_means, percentile)

return data_percentile

def my_pearsonr(est, X, y):

"""Use pearson correlation for validation score"""

y_pred = est.predict(X).squeeze()

# Use the numpy "corrcoef" function to calculate a correlation matrix

my_corrcoef_matrix = np.corrcoef(y_pred, y.squeeze())

# Return a single correlation value from the matrix

my_corrcoef = my_corrcoef_matrix[1, 0]

return my_corrcoef

本文仅使用了时间偏移特征以及岭回归构建机器学习模型,为获得更好的效果,可以使用更多的特征以及更复杂的回归算法。

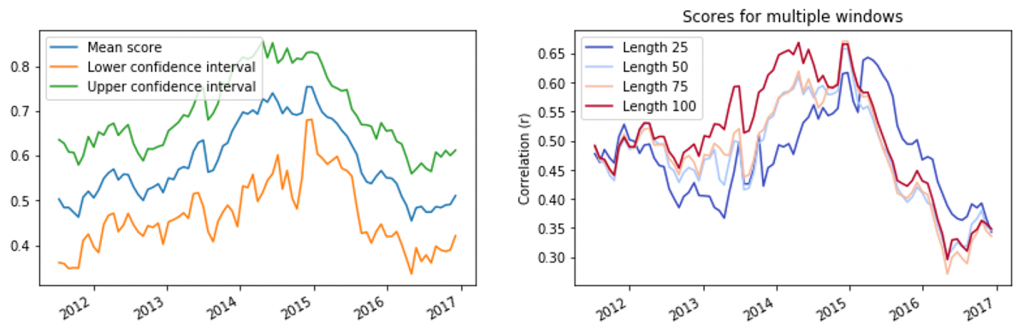

from sklearn.linear_model import Ridge from sklearn.model_selection import cross_val_score # Generate scores for each split to see how the model performs over time model = Ridge() cv = TimeSeriesSplit(n_splits=100) scores = cross_val_score(model, X, y, cv=cv, scoring=my_pearsonr) # Convert to a Pandas Series object scores_series = pd.Series(scores, name='score', index=scores_time) # Bootstrap a rolling confidence interval for the mean score scores_mean = scores_series.rolling(20).mean() scores_lo = scores_series.rolling(20).aggregate(partial(bootstrap_interval, percentile=2.5)) scores_hi = scores_series.rolling(20).aggregate(partial(bootstrap_interval, percentile=97.5)) # Plot the results fig, ax = plt.subplots() scores_mean.plot(ax=ax, label="Mean score") scores_lo.plot(ax=ax, label="Lower confidence interval") scores_hi.plot(ax=ax, label="Upper confidence interval") ax.legend() plt.show() #下方左图

在使用函数TimeSeriesSplit时,还可以通过定义参数max_train_size来限制每个验证集之前使用的训练样本个数:

# Pre-initialize window sizes

window_sizes = [25, 50, 75, 100]

# Create an empty DataFrame to collect the scores

all_scores = pd.DataFrame(index=scores_time)

# Generate scores for each split to see how the model performs over time

for window in window_sizes:

# Create cross-validation object using a limited lookback window

cv = TimeSeriesSplit(n_splits=100, max_train_size=window)

# Calculate scores across all CV splits and collect them in a DataFrame

this_scores = cross_val_score(model, X, y, cv=cv, scoring=my_pearsonr)

all_scores['Length {}'.format(window)] = this_scores

# Visualize the scores

ax = all_scores.rolling(20).mean().plot(cmap=plt.cm.coolwarm)

ax.set(title='Scores for multiple windows', ylabel='Correlation (r)')

plt.show() #下方右图

本文介绍了针对时间序列构造机器学习模型的常用方法,更高级和自动化的时间序列特征生成器可以参考tsfresh